What Does Home Equity Improvement Mean for Homeowners

- nevergiveup225

- 1 day ago

- 8 min read

Home equity improvement is the process of raising your home’s market value through strategic renovations while simultaneously reducing your mortgage balance to grow your ownership stake. Your equity is the difference between what your home is worth and what you still owe. Every dollar you add to that gap, whether through a kitchen remodel, a biweekly payment strategy, or a mortgage recast, directly strengthens your financial position. This guide covers the financial tools, high-ROI renovation projects, and payment strategies that homeowners and real estate investors can use to maximize equity in 2026.

What does home equity improvement mean and how does it work?

Home equity is defined as your home’s current market value minus your outstanding mortgage balance. If your home is worth $350,000 and you owe $220,000, your equity is $130,000. Home equity improvement means deliberately increasing that gap through two levers: raising the property’s appraised value and reducing the debt secured against it.

These two levers operate independently but compound when used together. A $25,000 kitchen remodel that adds $30,000 in appraised value increases equity by $30,000 on the value side. Paying an extra $200 per month toward principal reduces the debt side. Both moves widen the equity gap, and doing them simultaneously accelerates your net worth faster than either approach alone.

The industry distinguishes between two types of equity growth. Forced equity comes from renovations and principal paydown that you control directly. Natural equity comes from market appreciation and time. Smart homeowners target forced equity because it does not depend on market conditions outside their control.

The table below shows how these scenarios play out over five years on a $300,000 home with a $200,000 mortgage balance.

Scenario | Home Value (Year 5) | Mortgage Balance (Year 5) | Equity (Year 5) |

No improvements, standard payments | $330,000 | $188,000 | $142,000 |

Strategic renovations only | $360,000 | $188,000 | $172,000 |

Renovations plus extra principal payments | $360,000 | $175,000 | $185,000 |

The third scenario produces $43,000 more equity than doing nothing, without requiring a windfall or a refinance. That is the core argument for treating home equity improvement as a system, not a single project.

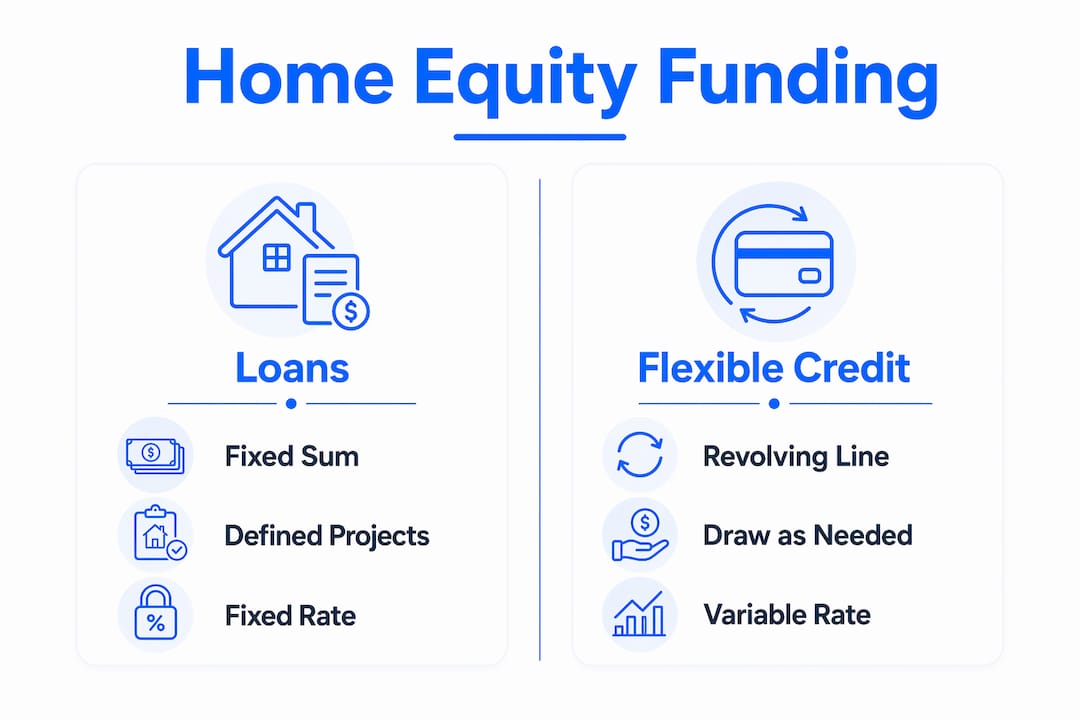

Which financial tools help you fund home equity improvements?

Homeowners have three primary financing tools for funding renovations: home equity loans, HELOCs, and mortgage recasts. Each serves a different renovation profile, and choosing the wrong one costs money.

A home equity loan delivers a fixed lump sum at a fixed interest rate. It works best for large, defined projects like a full bathroom renovation or a roof replacement where the total cost is known upfront. You borrow once, repay on a set schedule, and your monthly payment never changes.

A HELOC (Home Equity Line of Credit) functions as a revolving credit line. You draw funds as needed, repay, and draw again during the draw period. This structure suits phased projects or investors who are renovating multiple properties over time. The equity accessibility formula is straightforward: multiply your home’s current value by 80 to 90 percent, then subtract your mortgage balance. The result is the maximum you can typically borrow.

A mortgage recast is the most underused tool in this category. You make a large lump-sum payment toward principal, and your lender recalculates your monthly payment based on the lower balance. You keep your original interest rate and loan term structure, but your monthly obligation drops. Mortgage recasts are particularly effective for homeowners who receive a bonus, inheritance, or proceeds from a property sale.

Tool | Best for | Key advantage | Key risk |

Home equity loan | Single large project | Fixed rate, predictable payments | Less flexible if costs change |

HELOC | Phased or multiple projects | Draw only what you need | Variable rate exposure |

Mortgage recast | Lump-sum paydown | Lowers monthly payment, no refinance | Requires significant cash upfront |

One tax consideration applies to all three: interest is deductible only when the borrowed funds are used to buy, build, or substantially improve the property securing the loan. You must itemize deductions and keep detailed records of how renovation funds were spent.

Pro Tip: Match your financing tool to your renovation scope before you apply. A HELOC for a single defined project often leads to overspending because the credit line feels open-ended. A home equity loan creates a natural budget ceiling.

What are the most effective home equity improvements?

Not every renovation adds more value than it costs. The projects with the strongest return on investment share a common trait: they improve function, curb appeal, or livable space rather than personal taste.

Garage door replacement leads the 2026 ROI rankings, recovering up to 268% of project cost in added value. That figure sounds extreme, but it reflects how heavily buyers weight first impressions and curb appeal in competitive markets. Minor kitchen remodels recover up to 113% of cost, making them one of the few projects where you reliably get back more than you spend.

Beyond those headline numbers, the projects that consistently perform well include:

Bathroom renovations: Mid-range updates to fixtures, tile, and vanities recover 60 to 80% of cost and rank among the top buyer priorities.

Energy-efficient upgrades: New insulation, windows, and HVAC systems add appraiser value and reduce operating costs. Buildertrend experts specifically prioritize durable system upgrades over decorative trends for long-term equity gain.

Adding livable square footage: Finishing a basement or converting an attic to a bedroom adds measurable appraised value in most markets.

Exterior improvements: Fresh paint, landscaping, and a new front door consistently improve appraisals at low cost.

Projects that rarely recover their cost include luxury pool installations, high-end home theaters, and sunroom additions in cold climates. These upgrades serve lifestyle preferences but do not translate to proportional appraised value.

Over-improving relative to neighborhood standards is the most common and costly mistake homeowners make. A $150,000 kitchen renovation in a neighborhood where comparable homes sell for $280,000 will not push your appraisal to $430,000. Appraisers use neighborhood comps as a ceiling, not a floor.

Pro Tip: Before starting any renovation, pull three to five recent comparable sales in your neighborhood and identify the ceiling price. Then budget your project to bring your home up to that ceiling, not past it. Planning renovations with purpose from the start prevents the most expensive mistakes.

Always budget a 15 to 20% contingency for hidden costs. Plumbing surprises, outdated electrical panels, and structural issues discovered mid-project can consume your projected equity gain if you have not reserved funds to cover them.

How can homeowners accelerate equity growth beyond renovations?

Renovations raise your home’s value ceiling. Payment strategies lower your debt floor. The fastest equity growth comes from working both sides at once. Here are four financial moves that compound your results:

Switch to biweekly mortgage payments. Biweekly payments produce 13 full payments per year instead of 12, cutting approximately four years off a standard 30-year mortgage. The extra payment goes entirely to principal, accelerating equity growth without requiring a budget overhaul.

Apply windfalls directly to principal. Tax refunds, work bonuses, and inheritance proceeds applied to your mortgage balance reduce the debt side of your equity equation immediately. Even a single $5,000 principal payment early in a loan’s life eliminates years of interest and accelerates equity accumulation.

Request PMI removal at 20% equity. PMI removal frees $100 to $300 or more per month depending on your loan size. Redirecting that freed cash directly to principal creates a self-reinforcing cycle: lower balance, faster equity growth, better financial flexibility.

Time improvements to local market conditions. Renovating before a strong seller’s market peaks maximizes the appraised value your improvements capture. Staying informed on local inventory levels, median sale prices, and days-on-market data helps you decide when to invest and when to hold. Sequencing your projects strategically also prevents the cost overruns that come from doing work out of order.

Equity building is a long-term strategy that combines payments, improvements, and market timing. Homeowners who treat it as a system rather than a series of isolated decisions consistently outperform those who renovate reactively or make extra payments sporadically.

Key takeaways

Home equity improvement produces the strongest results when renovations, principal paydown, and market timing work together as a coordinated system rather than separate decisions.

Point | Details |

Equity defined | Home equity equals market value minus mortgage balance; both sides can be improved deliberately. |

Top ROI projects | Garage door replacement and minor kitchen remodels lead 2026 returns, recovering up to 268% and 113% respectively. |

Right financing tool | Match home equity loans, HELOCs, or mortgage recasts to your project scope to avoid overspending. |

Accelerate with payments | Biweekly payments add one full extra payment per year, cutting roughly four years from a 30-year mortgage. |

Avoid overcapitalization | Never renovate past your neighborhood’s comparable sale ceiling or you will not recover the cost. |

What I’ve learned after years of watching homeowners get this wrong

Most homeowners treat equity improvement as a renovation problem. They pick a project, hire a contractor, and hope the appraisal reflects their investment. That approach works sometimes, but it leaves too much to chance.

The homeowners I have seen build equity most consistently treat it as a financial discipline first and a renovation decision second. They know their current equity position, they know their neighborhood’s comp ceiling, and they have a payment strategy running in the background before they ever pick a paint color. The renovation is the accelerant, not the engine.

The most underused tool I keep recommending is the mortgage recast. Most homeowners have never heard of it. It does not require a new loan, does not reset your rate, and does not involve a credit check. If you receive a lump sum of any kind, a recast is often the highest-return move available, especially in a higher-rate environment where refinancing makes no sense.

I also want to be direct about hidden costs. I have seen too many homeowners plan a $40,000 renovation and end up at $58,000 because they skipped the contingency fund. That $18,000 overage did not come from bad luck. It came from not budgeting for what every experienced contractor knows is always there: the plumbing that needs rerouting, the subfloor that needs replacing, the electrical panel that is two decades past its service life. Build the contingency in before you start, not after you run out of money.

Finally, match your renovation to your timeline. If you are planning to sell within two years, focus on curb appeal, minor kitchen updates, and deferred maintenance. If you are staying for ten years, invest in durable systems and livable space. The right project at the wrong time is still the wrong project.

— Ricco

Ready to build equity with renovations that actually pay off?

Manycolorswi brings purposeful, skilled craftsmanship to every project, from flooring and drywall to painting and exterior work. Every job is completed by a trained team that takes pride in the work and the mission behind it.

If you are planning improvements to raise your home’s value, the team at Many Colors is ready to help you execute them the right way. Manycolorswi pairs professional results with a genuine commitment to community, meaning your renovation investment supports skilled workers who are building their own futures alongside yours. Reach out today to discuss your project and get a clear plan before the first nail goes in.

FAQ

What does home equity improvement mean exactly?

Home equity improvement means increasing the gap between your home’s market value and your mortgage balance through renovations, principal paydown, or both. The result is a larger ownership stake and greater financial flexibility.

Which renovations add the most home equity in 2026?

Garage door replacements and minor kitchen remodels lead 2026 ROI data, recovering up to 268% and 113% of project cost respectively. Energy-efficient upgrades and bathroom renovations also deliver consistent appraiser value.

Can I use a home equity loan to fund improvements?

Yes. A home equity loan provides a fixed lump sum at a fixed rate, making it well-suited for large, defined projects. Interest may be tax-deductible if the funds are used to substantially improve the property securing the loan.

How do biweekly payments improve home equity?

Biweekly payments produce 13 full mortgage payments per year instead of 12, directing one extra payment entirely to principal. This reduces your mortgage balance faster and shortens a 30-year loan by approximately four years.

What is the biggest mistake homeowners make with equity improvements?

Over-improving relative to neighborhood comparable sales is the most costly mistake. Appraisers use local comps as a value ceiling, so luxury upgrades in modest neighborhoods rarely recover their full cost even when they genuinely improve the home.

Recommended

Comments